Loading...

businessentrepreneurshipinvesting

How Infinite Banking Works | WealthWise Banking EP. 64

About this Episode

Website: www.WealthWiseBanking.com

LinkedIn: https://www.linkedin.com/company/wealthwise-banking

Many people hear about Infinite Banking and immediately wonder:

“How can my money still grow if I borrow against it?”

It’s a fair question.

In most financial accounts, when you use money, the balance drops and compounding slows.

So how does a properly structured whole life policy work differently?

In this episode, Jeremy and Jason break down the mechanism in plain English. You'll learn how money inside a policy becomes part of a large insurance company's balance sheet, how policy loans actually work, where the loan money really comes from, and why growth inside the policy can continue even when capital is deployed elsewhere.

No hype. No buzzwords. Just the mechanics.

If you want to see whether this type of capital structure belongs in your financial life, the next step is a Decision Readiness Review.

EPISODE HIGHLIGHTS

Intro - 00:00

The Biggest Misconception About Infinite Banking - 1:43

What “Uninterrupted Compound Growth” Really Means - 3:28

Where the Money Actually Goes Inside a Policy - 5:16

Why Borrowing From a Policy Doesn’t Stop Growth - 7:22

The Stability Behind Whole Life Policies - 11:16

The Real Purpose of Infinite Banking - 17:53

ABOUT YOUR HOSTS

At WealthWise Banking, hosts Jeremy Huggins and Jason Sipple combine decades of experience in finance, leadership, and wealth-building to help listeners eliminate debt, grow wealth, and build lasting legacies.

Jeremy, a West Point graduate and Special Operations Veteran, brings a strategic, disciplined approach to financial planning, shaped by years in high-pressure environments. Now a real estate investor, airline pilot, and certified Infinite Banking Concept Practitioner, he helps clients unlock financial freedom through IBC strategies designed for long-term stability.

Jason, a 5x Ironman Competitor, money mentor, and founder of Founding Fathers Financial, has guided thousands toward debt elimination, cash flow optimization, and legacy building. Through Founding Fathers, Jason leads a community of men focused on aligning wealth with purpose, fostering leadership, and building legacies that reflect their values.

Together, Jeremy and Jason share real stories of transformation, showcasing how listeners apply the Infinite Banking Concept (IBC) to take control of their financial futures.

Beyond the Mic: Jeremy enjoys fitness and outdoor adventures with his wife and two dogs, LB and Tito. Jason balances mentoring, Ironman training, and community-building through Founding Fathers.

🎧 Tune in weekly to learn practical strategies and simple shifts that unlock financial independence and lasting success.

Hosts & Guests

Transcript

I think the last one would be the tax treatment, okay?

So the growth, we do say it's tax deferred.

This is another thing that people kind of mis say,

are views out there.

The growth is actually tax deferred inside of policy loans.

It can be accessed tax-free because of the loan features.

It's very similar when you hear Elon Musk has billions of dollars in Tesla stock.

He doesn't pay any taxes because he's taken a policy loan against the stock.

Well, it's kind of very similar here.

You're taking the loan.

Loans are not taxable.

And therefore, you can access it tax-free.

Yeah, it's perfectly.

It is tax advantage, right?

Another way to say it.

So welcome to another episode of Wealth-wise Begging.

We've got some exciting news that we're going to unveil today.

We got someone else that has moved to the greatest country.

I mean, state in the world.

Jeremy Huggins, welcome to Florida, brother.

Yeah, yeah, thank you.

Thank you.

Made the official move yesterday.

That sounds miserable, actually.

Well, let's me get down here with you.

So a little bit more often, maybe we'll do some more in-person recordings.

I think it's going to be a really good thing.

I think it's going to be a lot of fun to have you down here.

You've got LB here.

My boys are excited.

We're all super excited to have you here, man.

So welcome to Florida.

Yeah, no, thanks, thanks.

And, you know, we're trying to figure out on this new episode.

What are we going to talk about on this show with me and my new move down here?

And we'll back and forth on, hey, should we do an episode for business owners or should

we do that?

We had that request from Nathan, right?

We had the request from your business partner, real estate partner, who told you, hey,

you guys are, you guys are giving us some pretty practical knowledge.

Yeah.

Right?

So, but the one thing that we keep getting is how does the whole thing work, right?

And so you've probably heard before with infinite banking, your money keeps growing even

when you use it.

And if you're intelligent, the objection I usually hear is, well, that sounds too good

to be true.

That is the most common thing I hear in all my calls, 4,000 plus calls.

It's too good to be true.

Yeah.

I thought the same thing.

Did you?

I did.

Yeah.

And that's why I went down the rabbit hole.

So, before we get into Nathan's suggestion on the next episode, I first want to talk about

this, right?

And too good to be true.

Your money keeps compounding even when you use it.

What is infinite banking?

How does it work?

Right?

So today, we're going to pull back the curtain, no hype, no magic.

We're just going to give a real simple explanation.

What is actually happening inside of a properly designed, whole life insurance policy and

what banks, family offices and large institutions use capital in this way?

Well, I think that the too good to be true part of it, right?

When people hear infinite banking, they wonder, how can I really grow my money if I'm borrowing

against it?

Like, how does that work?

Right?

Because that's not how traditional lending works.

That's not how we get money from a bank.

That's not what we even taught for the common path.

Yeah.

It's a fair question.

And most financial accounts, when you use your money, right, the balance drops to zero

and compounding slows.

So how does it work inside of a properly engineered policy?

And this episode today, we want to uncover that.

We want to go over that explanation and get rid of all the hype, no buzzwords, just the

mechanics of what's actually happening here.

And it's kind of stupid, simple.

Like I like to keep things simple like my last name.

So this is something where, whether wherever you are and you're deploying capital, you

need capital, you need an opportunity fund.

You need to understand these mechanisms and what we're going to be covering today.

Yeah.

All right.

So let's get into it.

So what is the most misunderstood phrase when it comes to infinite banking?

It is the uninterrupted compound growth.

Yeah.

And so a lot of smart people out there, they're suspicious.

I was suspicious, like you said.

You were suspicious about it.

I actually, I actually wasn't.

You weren't?

I wasn't, because I didn't have to poke holes in things.

I just, for 46 years, there's a problem in someone handed me a book and I read the book

and I was like, oh, why didn't anybody, I think tell me this.

Yeah.

So when this does happen, for most folks, they'll start going down the rabbit hole of how.

And that's, that's a fair question.

I think that's what leads a lot of people to misunderstanding of infinite banking, what

it's truly doing.

So when someone hears that I can borrow against a policy and the cash value keeps growing,

even if you borrow against it, well, how, how is it?

How is that actually happening?

Because it's not magic.

No, it's definitely not magic and people get stuck there too, because they think they

have, they get tired of the banks, right?

They get worn out, jumping through hoops, trying to say how much they make and how long

they've been at their job and all the different things to try to get capital when they need

it, when there's an opportunity.

And so now they hear why I can be my own bank and I can borrow my money, they think they're

borrowing their money, I can borrow my money and I can put it to work without any questions

asked.

And that's where some, some of it kind of falls apart for people is right in that thought.

Mm-hmm.

Can you catch that?

Yeah.

It's where if the objection happens, what happens next, right?

So people either shut down or they go down the rabbit hole of answering the question.

And it really has everything to do with how the insurance carers fill out their balance

sheets.

That's the true answer.

Yes.

Yes.

And what do we mean by that?

You go a little deeper into that?

Yeah.

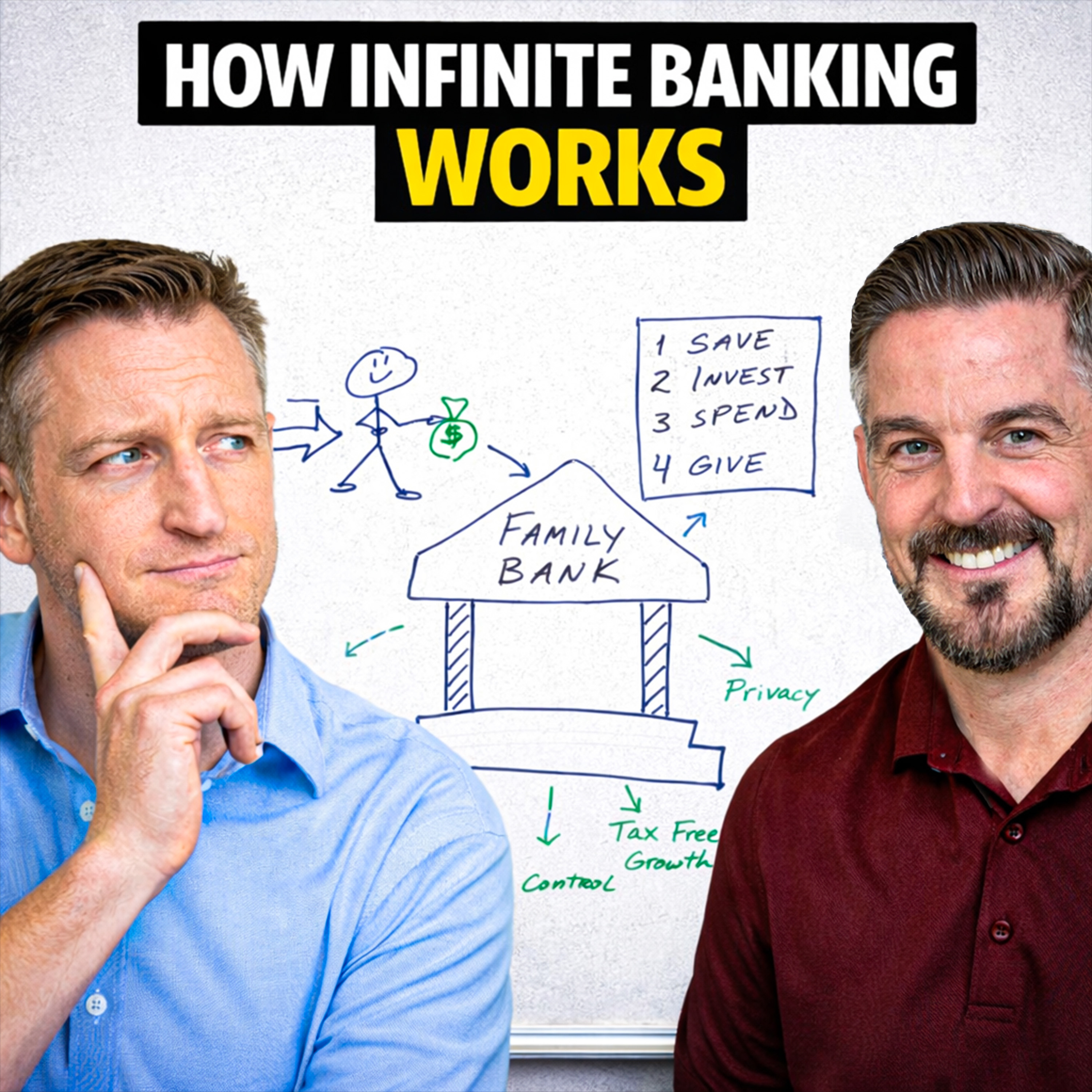

So when money enters into a policy, a properly engineered whole life policy, right?

It becomes part of the general account of the large mutual insurance carrier.

So we all have our own favorite mutual insurance carers are out there.

And these companies, well, they manage enormous amounts of capital, right?

Then they invest that capital into long-term institutional assets.

These include government bonds, corporate bonds, commercial real estate loans, right?

Like private lending.

Yeah.

I mean, you go to our favorite mutual companies and you drive around them and they start

pointing out buildings.

We own that building.

We own this, but we own that stadium, right?

They, then you go to infrastructure, financing.

You go into private credit.

You go into power, electricity, things that keep the country running.

They're investing in things that grow in a slow, predictable pattern.

Yeah.

Basically, stable assets that are designed to generate predictable returns over decades.

Okay?

So because of this structure, the company can then guarantee a minimum growth rate and

often they pay dividends.

And the companies that we like to work with have paid dividends every single year for over

100 years.

So the policy continues to grow whether or not you touch the capital.

And that's where people get a little bit.

So let's slow down here a little bit, even though this is very basic.

So the money, the premium deposit goes into a policy.

That's step one.

Someone gets approved, actually.

They get approved.

They put the policy in force.

They put their money into the system, right, this process we teach.

And now the money's there and then what happens?

So now that the money's there, the insurance care is investing it in the bonds, the institutional

assets, the private capital.

All of those features, all those different long term stable assets, that's what they're

investing in.

Yes.

And because they have to, they're guaranteeing, like when we sign a contract to have one

of these specially engineered policies, all of a sudden we're signing a contract that's

guaranteeing us a certain amount of growth year over year over year on all the cash value.

Correct.

That's correct.

And so once the policy builds cash value, it becomes an asset that the insurance company

can then lend against.

And that's where you, other people get another round of confusion, right?

You're not borrowing your own money.

You're not withdrawing your money.

You're actually borrowing against the policy using the cash value as collateral.

So a simple example would be, I have a policy with $100,000 of cash value.

Okay.

I take a policy loan of $40,000.

I'm borrowing their money.

So my $100,000 continues growing inside the policy.

Yeah.

If you're watching this, if you're not just listening and driving in the car, I'm holding

my hand up.

So you've got your capital, you're collateralizing, which is just a fancy word for borrowing

against this money.

And another point of confusion is to clear it up for people.

You can't borrow more than the cash value you have in a policy.

Right.

Some people, because you hear, hey, we're borrowing against the death benefit.

And they think, oh, I have a million dollar death benefit.

Even though I have $100,000 in policy cash value, I want to borrow a million.

No, you can borrow up against what amount of money you have as cash value.

Yeah.

So companies then lending their money, they're not removing yours.

And that's what allows the compounding to continue to grow, right?

Yeah.

We cover this in a lot of episodes.

We had a fun episode that your mom really liked.

Shout out to your mom.

It really liked the Ben Franklin episode where you have uninterrupted compounding year

every year and what that could look like in the millions and millions and millions of dollars

right for when he put in that was a thousand pounds of sterling.

Yep.

Sterling, today's dollars, $4,400 bucks.

Yeah.

And it ended up being should have been like $70 million, right?

But that uninterrupted compound, sorry, got sidetracked with the uninterrupted compounding.

The only place that I have ever found where you don't interrupt the compounding is with

one of these mutually owned dividend paying whole life insurance policies.

Yeah.

And then your policy simply acts as the collateral.

That's what's happening.

And you might have heard me say this before, I like to give my money three jobs, right?

I want to have my money saving where it's uninterrupted compounding tax-free.

I want to be able to spend the money.

I want to use other people's money like a line of credit.

That's what we're talking about today, that insurance company and I also like the fact

that my family's protected.

So I want to give that same dollar three jobs.

Yep.

Yeah.

So where the money actually comes from, okay?

This is another misconception that people end up having is that the money, the loan actually

comes from the policy balance sheet, right?

But it does it.

It actually comes from the insurance company's lending pool.

Yeah.

So your policy just secures the loan.

And that's very similar to like the HELOC against a house or a margin against a brokerage

account for all of our stock traders out there.

Yeah.

Again, it's just a line of credit.

You're borrowing against or collateralizing the asset.

It's pretty straightforward.

And when you look when we're talking about how the companies are guaranteeing things you're

talking about what they're investing, we're talking about large, like depending on the

size of the mutual company, we're talking about 30, 40, 50 million dollar portfolios that

are out working for them.

And usually the loan portion, it is something that's an asset to them.

It is something that they're making money on, but it's usually a really small portion,

like two to three to four percent, like most of the big mutuals that we know of.

It's a very, very small portion of their business because people also get nervous.

Well, if we're taking loans and collateralizing our loans and this is how they're making money,

how is it treated and all those types of things, right?

If you're practicing infinite banking, you're part of the rare.

It's more of a niche community so that the insurance carers are not being overwhelmed

with policy loans.

Yeah.

And that was kind of my point.

Because people ask me this week, hey, what are the insurance companies, and you covered

it already, what are the insurance companies, how can they be so stable?

How are they profitable for 100 plus years?

Yeah.

So we do have a couple layers of stability that are also built in, right?

So whole-life policies, they also add protection that many financial assets don't have.

And so for example, that guarantee for, right, that rate that you have, that's the growing

part of it.

That's the compounding that you get every single year.

And it happens regardless of what's going on in the markets.

We like to say that's non-market correlated.

So it doesn't matter what's going on the stock market, the housing market, all of that

is regardless.

So your growth still happens regardless what's going on.

I got dividends during COVID.

We talked to people who've had dividends going out from 9.11 and going out to 2008.com

bubble.

When I said dividends are paid out every single year for over 100 years without missing

a beat, that's what we're talking about.

These are very powerful companies.

Yeah.

We're talking 121 years, 137 years, 149 years, 160 years, 160 years.

These are the carriers that we know that we work with.

They're profitable every single year.

And Jeremy named a couple of recent things.

You can go back to the Great Depression.

You can go back to any of the World Wars.

You can go back to anything you can think of, whether it's financial, whether it's global,

whatever's going on, they're profitable.

And the reason why is because they're low risk, stable investments that compound slowly

over hundreds of years.

Yeah.

So we have a guaranteed growth rate.

Yeah.

That's a layer of stability.

We have a strong dividend history.

That's a layer of stability.

The next one, credit or protection.

I, as a real estate investor, love this asset, right?

So in many states, life insurance cash value is actually protected from lawsuits, bankruptcies,

creditors, divorces.

And guess where it's completely protected?

Where?

Some place that you just moved.

Over.

And 37 other states are fully protected, but it's always more protected than it would

be in your regular old bank.

Yeah.

And I think the last one would be the tax treatment, okay?

So the growth, we do say it's tax deferred.

This is another thing that people kind of miss say or abuse out there.

The growth is actually tax deferred inside of policy loans.

It can be accessed tax-free because of the loan features.

It's very similar when you hear Elon Musk has billions of dollars in Tesla stock.

He doesn't pay any taxes because he's taken a policy loan against the stock.

Well, it's kind of very similar here.

You're taking a loan.

Loans are not taxable.

And therefore, you can access it tax-free.

Yeah, it's perfectly.

It is tax-advanced, right, another way to say it.

And then why the capital enters the policy first?

Like this is one part for a lot of our investors, you know, the Nathan's of the world and other

folks that are builders, they're wondering like, hey, I can go make a bigger spread out

here.

Let's kind of hit that a little bit.

Yeah.

So when capital enters the policy first, what ends up changing the flow capital for a lot

of folks?

Well, for some, most people deploy capital like this.

You have money.

You throw it right into the investment or the deal, right, whatever opportunity that

you have.

But when you use infant and banking, where do you take your money first?

It goes from you to the policy.

You then take the policy loan and throw it into the investment.

That way the capital first receives protection, it receives guaranteed growth.

There's liquidity and compounding.

You get all of those features and benefits before the capital is being deployed elsewhere.

Yeah.

That's a little bit of a switch when we talk about how we're just changing one thing.

And the reason you want it running through your foundation first or your policy first is

because like Jeremy just said, it's protected.

It's guaranteed.

It's tax-free because investments, I mean, Jeremy is a pretty good investor, but there's

an open lid on investments.

Sometimes they work.

Sometimes they don't.

You got to really know and like what you're investing in.

So when you put this layer of protection like this is why I love it, Jeremy, I'm not

a good investor yet.

I will learn.

You will teach me.

I have made some investments.

I've done well here and there.

But at the same time, I'm building a really strong capital system.

So when I have liquidity in the future and like my mentor taught me is like Jason, I had

someone run off for the $100,000 I loaned them.

But guess what?

I can fill that back up.

That's still growing at the guaranteed rate.

That's still earning me dividends.

That's still protecting the people I love.

And it's still protecting and all the other things we just talked about.

There gives you a very strong financial foundation.

And when you have a strong financial foundation, you can go and invest more aggressively.

That's what way I look at it.

You like to be aggressive when you have stability first.

And this is something that I think a lot of people once they get in this, they say,

oh man, I thought it was too good to be true.

And then the next thing they say is, why did I know about this 20 years ago?

That's literally the next thing I hear.

And so the honest part that most people leave out is that the strategy's not magic.

There's always two things that are true, right?

The policy loans change our charge simple interest.

Policy growth is steady.

It's not stock market level, but it's steady.

It's consistent and never changes.

It's always going up.

So the real advantage is the capital efficiency.

You're not chasing the highest return.

You're looking for that stability first.

Anyone who's positioning infinite banking as an investment, run from that person, right?

This is a bridge between saving and investing.

Yeah, run is not an investment.

No, no, this is a different asset class.

And we didn't touch on one thing, but I had someone bring this up today where he said,

you know, I know I shouldn't trust the government in the banks,

but I just feel like because of the sticker on the on the window of the bank,

like, how is this protected, Jason?

I'm like, well, thankfully, it's not federally regulated.

It's state regulated.

It's protected like another part of a layer of this is there's guaranteed associations.

We're not here to talk about that today.

There's insurance on the insurance.

It's protecting the whole system, right?

So it's even more stable than then we're even letting on really.

So who would be a prime candidate for this, right?

So this approach works best for people who are already running businesses.

It works well for people who invest regularly.

It works well for people who recycle capital repeatedly, right?

And people who thank long term go figure.

That's what we talk about every single episode is thinking long term.

Yeah, thank long range, right?

And then this is why this same structure,

it appears other places like we see inside of banks and family offices,

large, large corporate balance sheets.

They know that it's there.

I mean, why do you think banks own so much of the stuff?

Tons, billions, billions of dollars.

Last time I checked, quarter four,

yeah, quarter, no, quarter three of 2024, it was $225 billion.

Yeah.

And you know, they bought more since then.

Mm-hmm.

Yeah, so the simple way to really understand this, folks,

a properly designed whole life policy

turns savings into collateralized capital, all right?

Your money continues compounding inside the policy

while the insurance company lends your money against it

to deploy elsewhere.

That's it.

That is what infinite making is.

That's the entire mechanism.

I'm pretty impressed that we just spend 20 some minutes

talking about basically you put the money in the thing,

you create a line of credit against it,

you borrow against it,

it's protected, it's guaranteed.

And you know, you have,

you have protection above and beyond what you had before.

That's what we just talked about for 20 minutes.

So most people think that the goal is finding the highest return,

but folks that are sophisticated,

they're looking for the uncommon path,

they ask a different question.

How do I keep my capital working in multiple places

at the same time?

The question I like to ask,

you guys can adopt this one,

is when that money gets spent,

you know, when you go to deploy that money,

will that money ever make me money again, right?

Like I wanted someplace where it's guaranteed to make me money

before I put it to work to make me money again.

Makes sense?

It's multiple jobs.

The same dollar has multiple jobs, at least.

So Jeremy, what's next?

Well, you know, if you're curious as to whether this type

of structure could improve the way that your capital flows,

the next step would just be a decision readiness review, right?

So what does that look like?

Go to WealthwiseBanking.com,

book a call with myself or Jason,

and we'll walk you through your current financial structure

and show you exactly where your capital sits,

how quickly it can move,

whether tools like this could actually improve your system,

and you can do that by, like I said,

going to WealthwiseBanking.com

and we have our calendars there.

That's it.

So as always, you know,

you're already in the business of banking.

You're just not the banker yet.

Jeremy, that was, thank you everybody.

Jeremy, that was a great time to have you back here in Florida.

And I'm looking forward to a lot of future episodes

with you here in Florida and the studio.

So, man, welcome back.

Welcome back.

Thanks.

We'll see you next week.

See you next week.

Thanks for joining us on WealthwiseBanking.

If today's episode inspired you, please subscribe,

leave a review, and give us a like.

It's a simple way to help others discover these empowering

strategies and join our community.

Together, we're building a network of people

who believe financial freedom is within everyone's reach.

Remember, financial independence

is about making every dollar work for you.

One step at a time.

Until next time, stay inspired, stay in control,

and keep building your legacy the wise way.

More from WealthWise Banking

View all episodes →

Artem Korolev: Why Systems Matter More Than Money | WealthWise Banking EP. 63

WealthWise Banking

Mar 4, 2026·32:15·pending

How High Earners Protect Future Income | WealthWise Banking EP. 62

WealthWise Banking

Feb 25, 2026·19:57·pending

From 4,400 to Millions: The Benjamin Franklin Story | WealthWise Banking EP. 61

WealthWise Banking