Loading...

newspolitics

Listen to This Article: Can Your Pension or Retirement Money Get Lost in the Bermuda Triangle?

About this Episode

This is a free preview of a paid episode. To hear more, visit www.racket.news

With the recent and ongoing "Software Apocalypse" we may just find out!

Narrated by Jared Moore

Hosts & Guests

Transcript

Can your pension or retirement money get lost in the Bermuda Triangle?

With a recent and ongoing software apocalypse, we may just find out.

It seems lately that every day when you read your morning paper, the business section has

another article about high net worth retail investors clamoring to get their money out

of private credit funds.

Funny, because it seemed like just yesterday, retail investors were clamoring to get in

on private credit funds.

The ongoing problems in private credit at first sound only like a Wall Street story,

a bunch of uber wealthy investors and powerful institutions screwing each other over and

taking a bath on their investments.

And taking a bath on their investments should happen every decade or so.

But it's not so simple.

Wall Street has been, Wall Street has spent years funneling Wall Street has spent years

funneling ordinary Americans long term savings into the private credit machine while paying

themselves to live in the style of Louis XIV in the process.

The Great Recession was bad.

But at least the basic story was visible.

Lenders push sketchy subprime mortgages that people couldn't repay, former homeowners

being kicked to the curb while banks, former homeowners being kicked to the curb while

banks made a fortune until it all imploded.

This time the danger is tucked inside opaque private funds and insurance vehicles marketed

as safe and secure.

Every day Americans, in other words, may not, in other words, may not realize until far too

late that their financial security was quietly wired into this pending blowup.

A huge meltdown in software industry stocks.

A huge meltdown in software industry stocks dubbed the SaaS spot, the SaaS pocket lips ripped

through $1.8 trillion private, dubbed the SaaS, dubbed the SaaS pocket lips ripped through,

dubbed the SaaS pocket lips ripped through the $1.8 trillion private credit industry.

Is it anthropic or anthropic?

Anthropic dubbed the SaaS pocket lips dubbed the SaaS pocket lips ripped through the $1.8

trillion private credit.

Dubbed the SaaS pocket lips ripped through the $1.8 trillion private credit industry last

month when anthropic released a new version of its large language model, LLM, Claude,

which highlighted the ease with which AI can automate software engineering.

The sell-off, the sell-off has hit private credit hard.

To get an idea of how brutal the software sell-off has been, consider the popular exchange

traded fund IG.

Consider the popular exchange traded fund IGV, which focuses on the software or SaaS vector,

which focuses on the software or SaaS vector, which focuses on the software or SaaS vector.

IGV began in 2026 at 107.28.

On February 23rd, it had dropped 28%, while it has recovered somewhat in March, 84.85 as

of March 16th, the anxiety around private credit remains.

Apollo Global Management President Jim Zelter told Bloomberg News that about 30% of private

equity firepower went into the-

and that software also accounted for roughly 40% of all-sponsored-backed private credit.

Recently, warnings came from other private equity private credit industry leaders.

I think that's a good idea to ask a question.

I think it's a good idea to ask a question.

I think that's a good idea to ask a question.

I think that's a good idea to ask a question.

I think that's a good idea to ask a question.

Recently, warnings came from other private equity private credit in it.

Recently, warnings came from other private equity in private credit industry leaders as

well.

Private market titans weren't a pain as credit cracks widen.

Investment markets

Investment markets people made choices.

If you wanted a higher dividend, you could take more risk.

You could lend to smaller companies.

You could run with a lot of leverage.

Apollo Global Management CEO Mark Rowan set on stage at the Bloomberg Invest Conference.

That felt really good on the way up.

That's not going to feel so good on the way down.

Rowan was among a chorus of executives warming of the additional troubles to come for the

industry.

Soros Fund Management Chief Investment Officer Don Fitzpatrick set investors in both

private credit and private equity are in for a painful 18 to 24 months.

Alternative asset management companies have heavily concentrated in software companies

because they previously provided predictable and high recurring revenue streams.

Additionally, software firms often have a sticky software firms often have a sticky customer

base as switching costs for users are expensive and highly inefficient.

These switching costs are often referred to as a defense.

These switching costs are often referred to as a defensive moat protecting the software

company from competition.

Suddenly, Anthropics lead as a version of Clawed has changed that logic.

Clawed's agentic or do it yourself capabilities.

Promise to pave over the moat by allowing developers to replicate complex existing software

code upending the software industry overnight and injecting fear into the private equity

and private credit universe.

To make matters worse for private credit portfolios, the software apocalypse was

bookended by the first brand's private credit fiasco in the fall.

And the current Iran war and energy crisis that had and the current Iran and the current

Iran war and energy crisis that has the potential to up in the entire economy.

And the current Iran war and energy crisis that has the potential to up in the entire economy.

Retail investors get the ball rolling down hill.

On February 18th, alternative asset management giant Blue Owl stopped investors from withdrawing

their money from one of its private credit funds, OBCD2.

OBCD2.

There was a run on.

There was a run on the fund amid investor concerns about the equity.

There was a run on the fund amid investor concerns about the credit quality and valuations

of the loans in the fund, especially as the software sector began to melt down.

This move, called gating, prompted such reactions as this from former...

Prompted reactions such as this from former PIMCO CEO, Muhammad Al-Aryan.

Is this a canary in the coal mine moment similar to August 2007?

This question will be on the mind of some investors and policymakers this morning, as

they assess the news that, quoting the FT, the private credit group Blue Owl will permanently

restrict investors from...

Blue Owl permanently halts redemptions at private credit fund aimed at retail investors.

To raise cash for investors wanting to exit and to pay down debt, Blue Owl sold

approximately $1.4 billion in loans for what it said was an average price of $99.

At or near $100 on the dollar, Blue Owl sold the loans to three pension funds, as well

as to its affiliate and insurance partner, Kuvare.

Kuvare

It's Kuvare, I think.

It didn't take long for the predators to start circling Blue Owl.

It didn't take long for the predators to start circling Blue Owl.

Saba Capital Management CEO, Boaz Weinstein, said he'd gladly take Blue Owl loans at

$65.80 on the dollar from retail investors to give them liquidity.

Saba Capital Management CEO, Boaz Weinstein, said he'd gladly take Blue Owl loans at

$65.80 on the dollar from retail investors to give them liquidity.

Weinstein, who has long been a critic of private credit, had this to say at an industry conference,

all you need is the snowball to start going down the hill and it started.

Blue Owl is right in the middle of that.

I think we are in the super early innings of the wheels coming off the car.

For many in the markets, Blue Owl sale to Kuvare raised suspicions that alternative

asset managers who oversee private loan funds while also managing affiliated US and offshore

insurance companies can move stressed assets from one entity to the other.

This can potentially mask the true market value of the assets.

More importantly, trades like the one between Blue Owl and its affiliated insurance company

can bury the risk within the insurance company's portfolio.

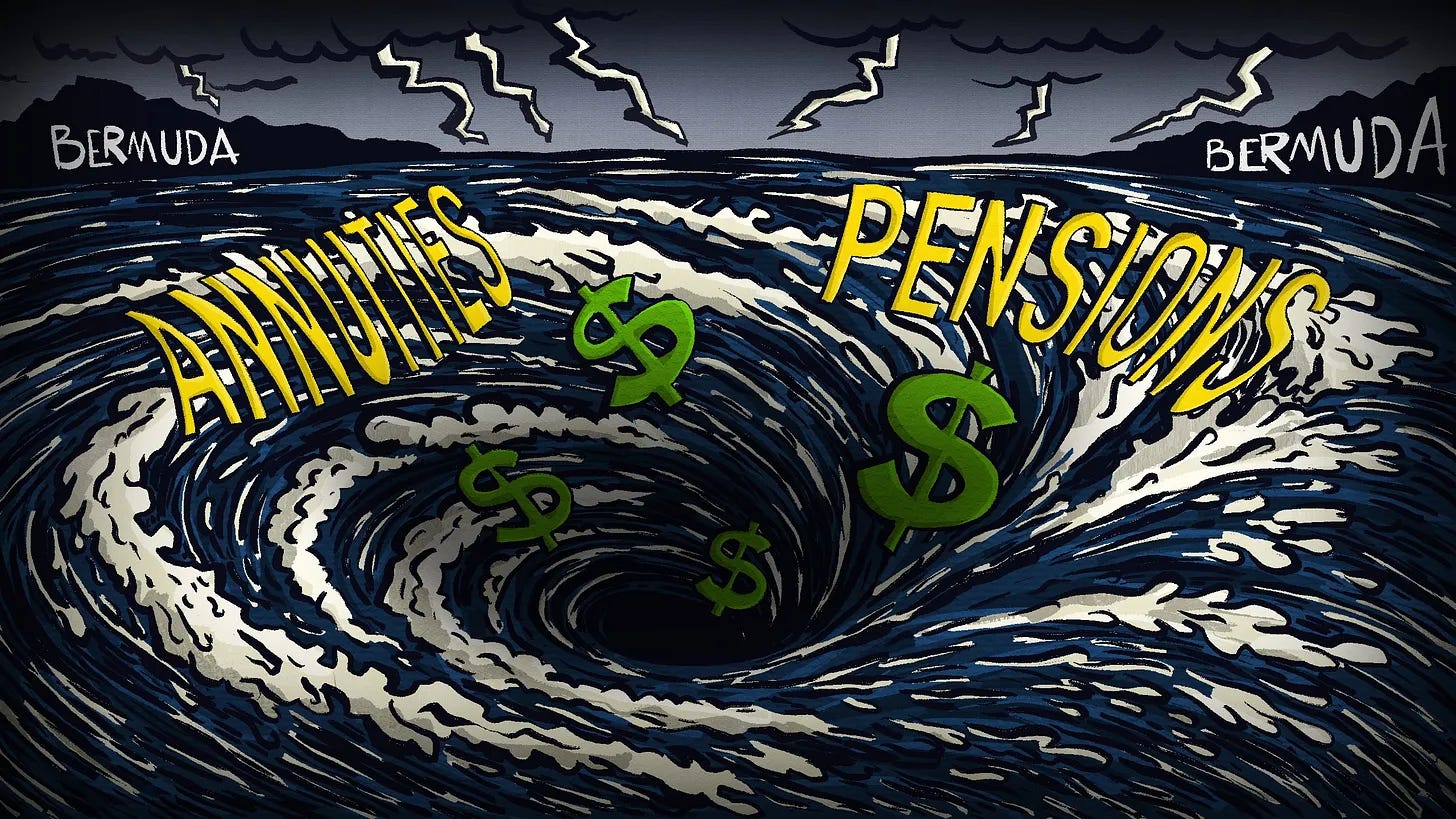

The portfolio that's backing annuity, the portfolio that's backing annuities and pensions,

the asset disappears in the Bermuda Triangle of finance.

The Bermuda Triangle

When I was a kid way back in the 1970s, we had a fascination with what was called.

When I was a kid way back in the 1970s, we had a fascination with what was called the

Bermuda Triangle, a mysterious body of water in the South Atlantic.

One of the wild stories about the triangle took place in 1944, when a squadron of five

Avenger torpedo bombers vanished over the Atlantic with just a final crackling radio transmission

from the lead pilot.

Everything looked strange, even the ocean.

We were obsessed with the phenomena, especially when the missing Avenger showed up in the

goby desert in one of our favorite movies, Close Encounters of the Third Kind.

Gradually, as time went on, pop culture left that version of the Bermuda Triangle behind.

However, thanks to alternative asset management companies, there's a new Bermuda Triangle.

As it turns out, you don't need a rift in the space-time continuum to make things disappear

in the Atlantic.

You just need a life insurance company in the U.S., an alternative asset manager, and

a re-insurance company, and a re-insurance company, insurance for the insurance companies,

in Bermuda.

In fact, there's a decent chance that if you have a pension or an annuity, you may already

be in this new Bermuda Triangle.

The Holy Grail for Private Assets The Holy Grail for Private Asset

Managers Such The Holy Grail for Private Asset

Managers Such It The Holy Grail for Private Asset Managers

Such As Apollo, KKR, KKR, Brookfield, Aries, Carlyle, Blackstone, and Blue Owl, is permanent

capital, a steady stream of investment capital, in one form of annuity and pension inflows.

Once captured, that money typically remains locked up for years, and can be deployed into

the manager's own private credit deals, private equity transactions, and even riskier

tranches of collateralized loan obligations made up of loans originated by the private

asset manager.

Made up of loans originated by the private asset manager.

No pain in the ass institutional limited partners bothering them about them.

No pain in the ass institutional limited partners bothering them about performance or demanding

their money back.

Rather, just a nice, quiet and compliant pool of funds from which the asset manager can

collect fees by putting the funds into the products they originate and earning the spread

between the annuity payments and the high-yielding investments.

In one form or another, Apollo, Blue Owl, Aries, KKR, Blackstone, Brookfield, and Carlyle

have built the triangle.

Some insurers, some own insurers outright, some partially, whatever their structure, they

all control the assets.

This is the way the triangle works.

A retail investor buys annuities from a life insurance company or an annuity provider,

or an entire corporation of pension, or an entire corporate pension fund transfers, or

an entire corporate pension fund transfers, pension risk transfer, or an entire corporate

pension fund transfers, pension risk transfer, its management to an alternative asset manager's

affiliated life insurance or annuity provider in the United States.

As the life company or annuity provider is affiliated or wholly owned by an asset

manager, the asset manager takes the funds and invests them in a product originated by

the asset manager.

It could be an investment in a private equity or private credit fund, or a number of the

other high-yielding illiquid alternative assets.

Meanwhile, the life company seeds the liability of the annuity to its affiliated reinsurance

company domiciled in Bermuda.

The asset manager puts the investment asset into the Bermuda re-insurance company where

there are far fewer capital requirements, money that is put aside for potential losses,

than in the US.

This juices the returns through leverage.

Shockingly, a tanned, rested, and retired former Goldman Sachs CEO, Lloyd Blankfein, recently

made clear to the Wall Street Journal that private credit industries greed is putting

people's life savings at risk.

If something blows up in big institutional investors' lose money, does the public sector

care that much?

Not really.

If a bunch of individuals start losing their 401k plans and their money, does the public

sector care?

Does the government sector care?

Does the government sector care?

Yes, a lot.

I think it's crazy to put those assets there, and I think it's crazy from their point

of view.

They have nice lives, they make a fortune.

Their companies are huge.

They already own their yachts.

They already own their yachts and whatever it is they want.

Why are you going into this dangerous territory just to make your business a little bigger?

Why are you going into this dangerous territory just to make your business a little bigger

when that represents such a big potential problem in the future?

These securities are opaque and may be riskier than most, but to the extent you're selling

to institutions people don't care that much.

But to the extent you're selling to institutions, people don't care that much.

But if individuals lose money or insurance companies are real businesses lose money,

it's terrible.

That's a bit of sobering statement from a former CEO of Goldman Sachs.

However, not heating blankfine's advice, Apollo Global Management has already gone in

full.

Apollo Global Management has already gone in full bore for the holy grail of permanent

capital.

In 2022, Apollo completed its purchase at a, Apollo completed its purchase of a theme,

the largest US annu- the largest US annuity provider for both retail and pension funds.

For both retail investors and pension funds, Athene also has a Bermuda re-insurance company.

Apollo invests Athene's assets and direct loans it originates to private companies in

collateralized loan obligations, CLOs backed by Apollo originated debt.

And in Apollo's and in Apollo's private credit funds.

As of June 2025, these investments totaled $44 billion.

In an August 2025 presentation, Athene highlights the Apollo relationship in great detail.

By investing in private loans over publicly traded loans, Athene can earn 100-200 basis.

Athene can earn 100-200 basis points and higher yields.

They give up liquidity, the ability to sell the asset relatively quickly without a substantial

hit-to-market value.

But they are rewarded with higher yields by taking on complex assets such as middle-market

CLOs that take longer to sell.

This strategy carries a lot of risk.

AMBest, a credit rating firm that focuses on the insurance industry, published a pay

walled report this past December that found PE AM backed insurers are taking on more

investment risks built on the experience of their parent companies' instruction products,

mortgages, private credit and other alternatives.

However, concerns arise around exposure growth, inter-organizational concentration, collateral

and valuations.

The report also flagged the growing reliance on private equity.

The report also flagged the growing reliance on private letter ratings, PLRs.

Unlike a public credit rating from Moody's or S&P that anyone can look up, a PLR is a

secret grade issued by a rating agency directly to the insurance company.

A good rating means insurers can hold less capital against the asset, which frees up cash

to buy more private assets, what could possibly go wrong?

Finally, AMBest states that as of December 2024, affiliated investments as a percentage

of capital, affiliated investments as a percentage of capital and surplus, affiliated investments

as a percentage of capital and surplus have sharply risen to 76% in 2024 from 45% in 2018

for those companies with affiliated investments.

In a world where Apollo's Mark Rowan admits a shakeout is coming, having three quarters

of safety net tied up in your own family deals is a massive systemic risk.

If the parent company's deals go south, the insurance company doesn't just lose its investment,

it loses its capital.

Finally, just how permanent is that permanent capital?

Just how permanent is that permanent capital?

As stated earlier, asset management firms go after insurance companies and pension transfers

because their money is considered sticky.

An annuity holder has to pay up to an annuity holder has to pay up to a 10% surrendered charge

to get their money out.

They assume that rational people won't throw away 10% of their life savings just to get

out early.

I'm not quite sure what the answer is here.

I feel like I did in late 2006 or early 2007 when I sat on a Wall Street trading desk

realizing that terrible mortgage loans had been made.

The bonds and the derivatives had been created and sold and that there was nothing to do

but wait for an explosion and pray for survival and pray for survival.

Thanks for listening to the audio version of this article.

For more, visit racquet.niz.